Taking a tech breather

Author: Pieter Schop, Senior Portfolio Manager Equity Specialties and Manager Information Technology at NN Investment Partners

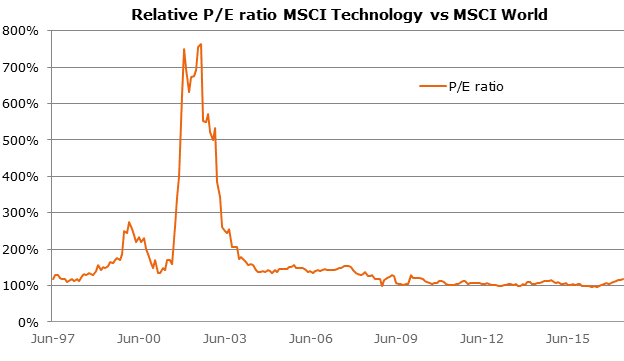

Global technology shares have outperformed the broader equity index by a third over the last 3 years. This has been driven by great investor appetite for big non-cyclical themes, like artificial intelligence, autonomous driving, the cloud, big data and Internet of Things. However, unlike the technology boom at the end of 1990’s, the upswing in technology shares has been driven by upgrades of analysts’ earnings estimates rather than built on thin air. We believe the technology sector remains a healthy place for investors and valuations are aligned with growth prospects. We see the recent correction as nothing more than profit taking and not driven by fundamentals. Earnings growth for the technology sector has been superior and will most probably remain superior for the foreseeable future. The past 10 years have seen mobile phones go from being $50 calling and texting devices to $500 mobile supercomputers. Society and institutions are just starting to adjust to this new reality. Autos, retail and health care are sowing the seeds of a new cycle of technology penetration. This better than expected earnings growth has driven upgrades, causing the shares to perform well. The price-earnings ratio (P/E) multiple expansion has been roughly in line with the market, as can be seen in the graph below.

Technology shares trade only at a slight premium to the market and are nothing like the levels we have seen in the late 1990’s, when the sector was trading at a large premium. Low inflation expectations and low interest rates have resulted in a rally in growth stocks, creating a place where stocks are vulnerable to profit taking. This stock price volatility has been highest for the most crowded and most expensive stocks. While people may be afraid the rally is about to end, bond markets continue to price in subdued economic growth. In an environment of low economic growth and deflationary pressures, growth stocks will continue to perform well due to their scarcity value. Furthermore, valuation of technology companies is attractive compared to the growth potential, innovation is abundant, balance sheets are strong and earnings momentum remains good. We are optimistic about the ability of the sector to outperform the broader market going forward and we are convinced that the longer-term prospects for the technology sector remain bright as the sector will continue to play an important role in productivity gains within the broader economy.